Beyond Hardware: Apple’s silent margin giant.

Company Overview

Apple needs little introduction: it is one of the few brands in the world capable of transforming consumer products into a global ecosystem with exceptionally high customer loyalty. The Group designs, manufactures, and markets digital devices and solutions, building an integrated ecosystem that combines consumer hardware with high-value-added recurring services. Founded in 1976 and headquartered in Cupertino, California, the company formalized its evolution beyond the personal computer by changing its name from Apple Computer, Inc. to Apple Inc. in January 2007. Its product lineup includes the iPhone, Mac, and iPad, as well as the Wearables, Home & Accessories division, which encompasses Apple Watch, AirPods, Apple Vision Pro, Apple TV, HomePod, and both Apple and third-party accessories (including Beats products).

In parallel, the Services segment has become a structural pillar of profitability and retention. This is driven by assets such as the App Store and digital platforms for app and content distribution (music, video, games, podcasts, books), AppleCare, cloud services, payment and financial solutions (Apple Pay, Apple Card), and a growing subscription portfolio (Apple Music, Apple TV+, Apple Arcade, Apple Fitness+, Apple News+), alongside advertising initiatives and licensing/IP monetization agreements. The company serves consumers, SMEs, and institutional markets (education, enterprise, and government) through an omnichannel distribution strategy that combines proprietary retail and online stores, a direct sales force, and third-party channels (network operators and resellers).

Business Lines

Apple’s business model can be viewed as a dual-engine system: on one hand, a Products portfolio that builds and refreshes the installed base; on the other, a Services layer that increasingly monetizes that base with a structurally superior economic profile.

Regarding Products, Apple designs and sells iPhone, Mac, iPad, and the Wearables, Home & Accessories category (Apple Watch, AirPods, Apple Vision Pro, Apple TV, HomePod, and accessories).

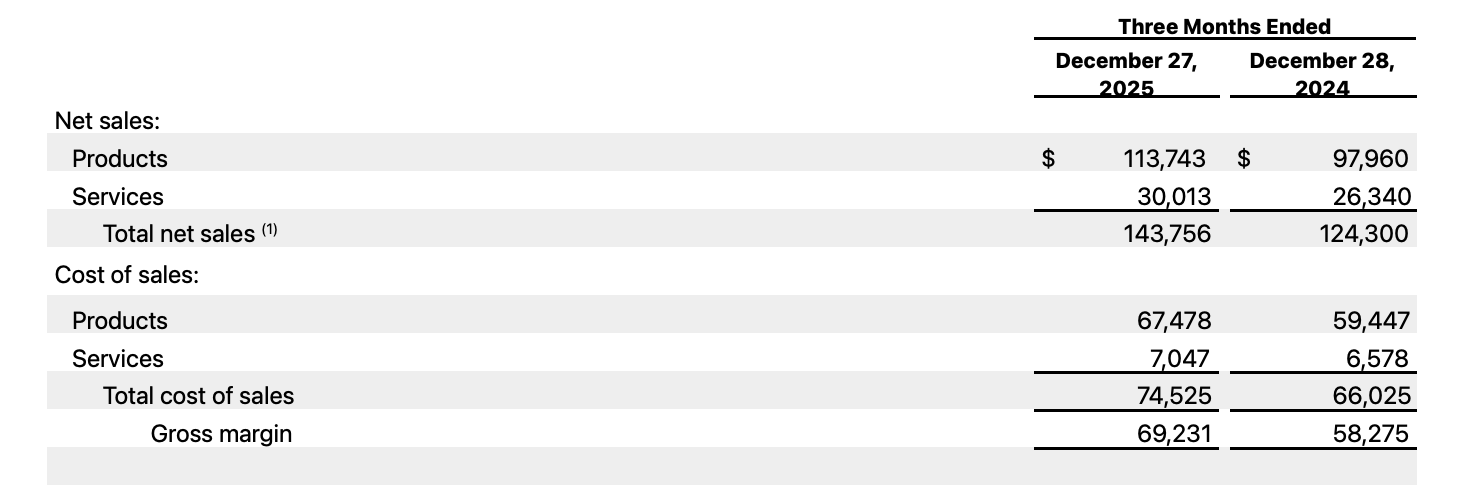

In Q1 FY2026, hardware remains the primary volume driver: Products account for approximately 74% of revenue (73.77%), while Services contribute roughly 26% (26.22%).

However, the perspective shifts when analyzing the quality of revenue. Despite accounting for the majority of total sales, the Products segment yields a gross margin of approximately 40%, consistent with the higher cost structure inherent in hardware manufacturing and supply chain management.

In contrast, Services, while representing a smaller share of total revenue, delivers a gross margin of roughly 77%. This is driven by a highly scalable, asset-light model encompassing digital platforms, subscriptions, content distribution, cloud services, and support. This asymmetry explains why the expansion of services within the Apple ecosystem has consistently pushed the Group’s overall profitability upward; for the quarter, the consolidated gross margin stands at approximately 48%.

Crucially, these two engines are interdependent: hardware is the prerequisite for selling services. Each additional iPhone, Mac, or iPad is not merely a one-time sale, but a new “user within the perimeter” (the Apple ecosystem). Over time, these users tend to activate proprietary services, such as payments, storage, media subscriptions, the App Store, and AppleCare, increasing the likelihood of recurring revenue and growing monetization per device.